4 Reporting

4.1 Reporting Principles and Requirements

4.1.1 GAAP Reporting Requirements

4.1.1.10 GAAP reporting requirements

The requirements for financial reporting in accordance with generally accepted accounting principles (GAAP) are established by the Governmental Accounting Standards Board (GASB) in the GASB Statement 34, Basic Financial Statements – and Management’s Discussion and Analysis – for State and Local Governments.

The following diagram illustrates the minimum requirements for general purpose external financial reports.

4.1.1.20 Comparative financial statements mean two complete sets of financial statements for each comparative year. Each set should contain basic financial statements (including notes) and RSI (including MD&A). Both years may be combined in one presentation; however, each element (MD&A, basic financial statements, notes and RSI) have to include information for both years.

1. Management Discussion and Analysis (MD&A)

4.1.1.30 MD&A should introduce the basic financial statements and provide an analytical overview of the local government’s financial activities. It is part of the Required Supplementary Information (RSI), however it should be presented before the basic financial statements. The MD&A should provide an objective and easily readable analysis of the local government’s financial activities. It should include comparisons of current year to the prior year based on the government-wide information. It also includes information regarding the local government budget variances, capital assets, long-term debt activity, and a description of currently known facts, decisions, or conditions expected to have a significant effect on financial position or results of operations.

2. Basic financial statements

Government-wide financial statements

4.1.1.40 The government-wide financial statements consist of a Statement of Net Position and a Statement of Activities. They are prepared using the economic resources measurement focus and the accrual basis of accounting. Each statement distinguishes between the governmental and business-type activities of the primary government and its discretely presented component units.

Statement of Net Position

4.1.1.50 The Statement of Net Position presents the local government as one economic unit rather than a compilation of different funds. The statement focuses on type of activities, rather than type of funds. Local governments should report all capital assets, including infrastructure assets in the government-wide statement of net position. The net position should be reported in three categories: net investment in capital assets, restricted and unrestricted.

Statement of Activities

4.1.1.60 The Statement of Activities is a report on the results of the local government’s operations. The statement presents the cost of each function and the extent to which each of the local government’s functions, programs or services either contributes to or takes away from the local government’s general revenue.

The required format provides:

- Information indicating the extent to which current-year program revenues supported the cost of the current-year services, and

- How the local government finances its activities.

Fund financial statements

Governmental Fund Financial Statements

4.1.1.70 Governmental funds should be reported using the current financial resources measurement focus and the modified accrual basis of accounting. These funds are presented by general fund; major funds, and aggregated nonmajor funds.

There are two statements required - the Balance Sheet and the Statement of Revenues, Expenditures and Changes in Fund Balance. General capital assets and general long-term liabilities are not reported in the governmental fund balance sheet. (They are reported in the government-wide financial statements.)

4.1.1.80 The Statement of Revenues, Expenditures and Changes in Fund Balance reports information about the inflows, outflows, and balances of current financial resources of each major governmental fund and for the nonmajor governmental funds in the aggregate.

4.1.1.90 Each statement reports separate columns for the general fund and for other major governmental and enterprise funds. Major funds are funds whose revenues, expenditures/expenses, assets, or liabilities (excluding extraordinary items) are at least 10 percent of corresponding element totals for all funds of that category or type and at least five percent of the corresponding element total for all governmental or enterprise funds combined. The local government may choose to report any other funds as a major fund if they believe they are important to users. The nonmajor funds are reported in aggregate in a separate column.

Proprietary funds financial statements

4.1.1.100 There are three required fund financial statements for proprietary funds:

- Statement of Net Position,

- Statement of Revenues, Expenses and Changes in Fund Net Position, and

- Statement of Cash Flows

4.1.1.110 Proprietary funds continue to be presented on the economic resources measurement focus and the full accrual basis of accounting. Proprietary funds are reported the same way as in the government-wide financial statements. However, internal service funds should be reported as a fund type (aggregated) in a separate column. Major enterprise funds are reported in separate columns and nonmajor enterprise funds are aggregated in a single column.

4.1.1.120 The proprietary Statement of Net Position presents assets and liabilities in a classified format. Restricted assets are reported separately. Net position should be reported in the following three components: net investment in capital assets, restricted and unrestricted.

4.1.1.130 The proprietary Statement of Revenues, Expenses, and Changes in Fund Net Position reports in a specific format prescribed by the GASB Statement 34. All transactions that affect net position are included. Revenues are reported by major source. Expenses are reported by either detail (object) or function level. Revenues and expenses should distinguish between operating and nonoperating.

Fiduciary fund financial statements

4.1.1.140 The following are required financial statements for fiduciary funds:

- Statement of Fiduciary Net Position, and

- Statement of Changes in Fiduciary Net Position

The fiduciary statements are prepared using the economic resources measurement focus and full accrual basis of accounting (with some exceptions for liabilities for defined benefit pension plans and certain postemployment health care plans).

4.1.1.160 The Statement of Fiduciary Net Position should include information about the assets, liabilities, and net position for each fiduciary fund type and for similarly discretely presented component units of the reporting entity. The local government should provide details for all other fiduciary funds, or clearly indicate where the information is displayed.

4.1.1.170 The Statement of Changes in Fiduciary Net Position should include information about the additions to, deductions from, and net increase (or decrease) for the year in net position for each fiduciary fund type and similar discretely presented component units. It should provide information about significant year-to-year changes in net position. The local government should provide additional details about investments and provide the level of details for all other fiduciary funds or clearly indicate where the information is displayed.

3. Notes to the financial statements

4.1.1.180 Notes to the financial statements are essential to fair presentation of the basic financial statements. The notes include the summary of significant accounting policies and summary disclosure of such matters as significant contingent liabilities, encumbrances outstanding, significant effects of subsequent events, pension plans, accumulated unpaid employee benefits (such as vacation and sick leave), material violations of finance-related legal and contractual provisions, debt service requirements to maturity, commitments under noncapitalized leases, construction and other significant commitments, any excess of expenditures over appropriations in individual funds, deficit balances of individual funds, and interfund receivables and payables. Any other disclosures necessary in the circumstances should also be included.

The NCGA has discussed the notes to financial statements in more detail in its Interpretation 6, which also provides guidance for presenting notes in a logical order.

4. Required Supplementary Information (RSI)

4.1.1.190 Statements, schedules, statistical data, and other information the GASB deem necessary is reported as required supplementary information (RSI). Except for the MD&A, required supplementary information, including the budgetary comparison information, should be presented immediately following the notes to the financial statements.

There are four types of RSI (other than MD&A) that must be presented:

- Budgetary comparisons (for the general fund and other individual special revenue funds),

- Infrastructure condition and maintenance data (for local governments using the modified approach),

- Pension trend data (for certain pension plans and participating employers),

- Revenue and claims development trend data (for public-entity risk pools).

Reporting Entity

4.1.1.200 GASB Statement 14, as amended by Statements 34, 39, 61, 84, 90 and 97 establishes standards for defining and reporting on the financial reporting entity and applies to financial reporting by primary governments, as well as to separately issued financial statements of governmental component units. The standards and its amendments are codified in GASB Codification section 2100 Defining the Financial Reporting Entity and section 2600 Reporting Entity and Component Unit Presentation and Disclosure. These sections define the financial reporting entity as consisting of (1) the primary government, (2) organizations for which the primary government is financially accountable and (3) other organizations for which the nature and significance of their relationship with the primary government are such that exclusion would cause the reporting entity’s financial statements to be misleading or incomplete.

4.1.1.210 As described in GASB Codification 2100, a primary government is financially accountable for a separate legal entity – and therefore should include the entity in its financial statements – in the following circumstances:

a. The primary government is financially accountable if it appoints a voting majority of the organization’s governing body and (1) it is able to impose its will on that organization or (2) there is a potential for the organization to provide specific financial benefits to, or impose specific financial burdens on, the primary government.

b. The primary government is financially accountable if a special purpose district is fiscally dependent on the primary government and there is a potential for the special purpose district to provide specific financial benefits to, or impose specific financial burdens on, the primary government, regardless of whether the special purpose district has (1) a separately elected governing board, (2) a governing board appointed by higher level of government, or (3) a jointly appointed board.

c. The primary government is financially accountable for a legally separate organization if the primary government holds a majority equity interest in an organization that does not meet the definition of an investment.

4.1.1.220 Component units should be reported in the financial statements of the primary government by either discrete presentation or blended presentation based on. Discrete presentation involves reporting the component unit in separate columns on the government wide statements. Blended presentation involves reporting the component unit’s balances and transactions as if they were part of the primary government in both the fund level and government wide statements.

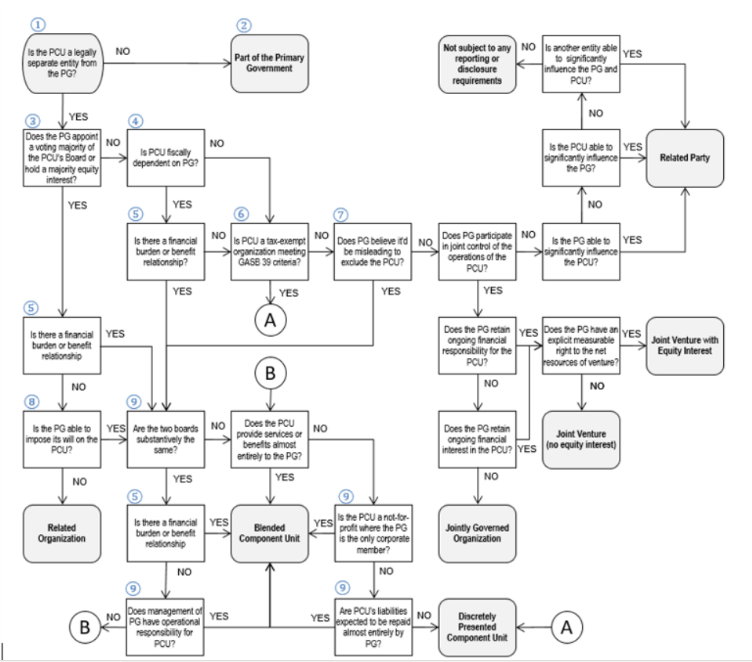

The following flowchart will help to determine the reporting status of an organization. Refer to GASB Codification section 2100 for definitions of the various terms.

4.1.1.230 In September 2006, GASB issued the Statement 48, Sales and Pledges of Receivables and Future Revenues and Intra-Entity Transfers of Assets and Future Revenues. This Statement applies to all intra-entity transactions (sales and donations) that involve the transfer of financial assets, capital assets and future revenues.

When accounting for the transfer of capital and financial assets and future revenues within the same financial reporting entity, the transferee should recognize the assets or future revenues received at the carrying value of the transferor. The difference between the amount paid (exclusive of amounts that may be refundable) and the carrying value of the assets transferred should be reported as a gain or loss by the transferor (revenue in governmental funds) and as a revenue or expenditure/expense by the transferee in a separately-issued statements, but reclassified as transfers in the financial statements of the reporting entity. Application of this Statement should be the same for both discretely presented and blended component units.

4.1.1.240 Hospital districts: The General Accounting Standards Board (GASB) Codification of Governmental Accounting and Financial Reporting Standards, section Ho5.601 supersedes the June 1996 AICPA Audit and Accounting Guide, Health Care Organizations, to the extent of financial reporting. However, the Guide continues to provide guidance on individual transactions that are unique to healthcare organizations. The Guide is considered Category B guidance in the hierarchy of GAAP.

Financial Reporting Entity Flowchart

Notes to Financial Reporting Entity Flowchart

PG = primary government (the government preparing financial statements)

PCU = potential component unit (the entity under consideration)

1. An organization has separate legal standing if it is created as a corporate or a corporate body possessing the corporate powers that would distinguish it as being legally separate from the primary government (such as the right to sue and be sued in its own name, hold or lease property in its own name, loan money or open a bank account in its own name and with its own tax or other identification number, etc.). For example, a government may have advisory committees or councils which are not incorporated as separate legal entities, or a government may participate in cost sharing projects or joint purchasing arrangements or other contractually coordinated efforts with other governments that (see GASB Codification J50.115). All funds, organizational units, agencies, departments, offices and activities of an organization that are not legally separate are, for financial reporting purposes, considered part of a primary government.

2. If the activity or operation is not separate legal entity, it should be reported as part of the government. For example, departments, projects, committees or initiatives of the government may have distinct branding, purposes or management structures within the government, but for reporting purposes would be reflected using appropriate accounting as part of the government’s funds. As discussed in GASB Codification J50.114, a government may have an arrangement that resembles a joint venture but has no separate entity or organization created by the participants. In such a joint operation (or undivided interest), each participant reports their own assets, liabilities and activity since there is no separate organization to hold property or incur obligations.

3. With regard to a voting majority, the primary government’s appointment authority should be substantive and continuing. A primary government’s appointment authority may not be substantive if candidates are limited by a nominating process or if its responsibility is limited to confirming appointments made by individuals or groups other than the primary government’s officials or appointees. In the absence of continuing appointment authority, the ability of a primary government to unilaterally abolish an organization also provides the basis for ongoing accountability. If the primary government performs the duties of a governing board, it would be considered the same as appointment of a voting majority, with the exception of a potential component unit that is a defined contribution pension plan, defined contribution other post-employment benefit plan, or other employee benefit plan (e.g., a 401k, 401a, 403b or 457 plan). In addition, the primary government would also be considered financially responsible if it held a majority equity interest in the entity, regardless of control, unless equity interest would be more appropriately classified as an investment (that is, unless the equity interest is held primarily for purpose of income and has a present service capacity based solely on its ability to generate or be sold for cash).

4. An organization is fiscally dependent if it cannot meet all three of the following requirements without substantive approval of a primary government:

a. Determine it budget,

b. Levy taxes or set rates or charges, and

c. Issue bonded debt.

It is also important to make a distinction between substantive and ministerial (compliance) approval. Ministerial approval is often a result of the general oversight of the respective state or local governments. This may include evaluation of programs, review for compliance with the statutory requirements, etc. Being subject to ministerial approval does not qualify an organization as fiscally dependent. Also, a primary government that is temporarily under the fiscal control of another government continues to be fiscally independent.

5. The benefit or burden relationship may result from legal entitlements or obligations, or it may be less formalized and exist because of a decision made by the primary government or agreements between the primary government and component unit.

An organization has a financial benefit or burden relationship with the primary government if any one of these conditions exists, either directly or indirectly:

a. The primary government is legally entitled to or can otherwise access the organization’s resources.

b. The primary government is legally obligated or has otherwise assumed the obligation to finance deficits of, or provide financial support to, the organization.

c. The primary government is obligated in some manner for the debt of the organization.

Exchange transactions between organizations and the primary government are not considered a financial benefit or burden relationship.

6. Certain organizations warrant inclusion because of the nature and significance of their relationship with the primary government, including their ongoing financial support of the primary government or its other component units. A legally separate, tax exempt organization (e.g., foundation or association) should be reported as a discretely presented component unit if all of the following criteria are met:

a. The economic resources received or held by the organization are almost entirely for the direct benefit of the primary government, its component units, or its constituents.

b. The primary government is entitles to, or has the ability to otherwise access, a majority of the economic resources received or held by the separate organization.

c. The economic resources received or held by an individual organization that the specific primary government, or its component units, is entitled to, or has the ability to otherwise access, are significant to that primary government.

7. Other organizations should be evaluated as potential component units if they are closely related to or financially integrated with the primary government and included as component units if the nature and significance of their relationship with the primary governments is such that exclusion from the financial reporting entity would render the financial statements incomplete or misleading. It is a matter of professional judgment to determine whether the nature and the significance of a potential component unit’s relationship with the primary government warrant inclusion.

8. A primary government has the ability to impose its will on an organization if it can significantly influence the programs, projects, activities, or level of services performed or provided by the organization. The existence of any one of the following abilities indicates that the primary government has the ability to impose its will on an organization:

a. Ability to remove the appointed members of the organization’s governing body at will.

b. Ability to modify or approve the budget of the organization.

c. Ability to modify or approve the rate or fee changes affective revenues, such as water usage rate increases.

d. Ability to veto, overrule, or modify the decisions (other than those in b and c) of the organization’s governing body.

e. Ability to appoint, hire, reassign, or dismiss those persons responsible for the day-to-day operations (management) of the organization.

There may be other conditions indicating the imposition of will. When assessing them, remember to make the distinction between substantive and ministerial approvals.

A potential component unit for which a primary government is financially accountable may be fiscally dependent on another government. An organization should be included as a component unit of only one reporting entity. Professional judgment should be used to determine the most appropriate reporting entity. A primary government that appoints a voting majority of the governing board of a component unit of another government should make the disclosures required for related organizations.

9. A component unit should be presented as blended in any of the following circumstances:

a. When the component unit’s governing body is substantively the same as the governing body of the primary government and (1) there is a financial benefit/burden relationship between the primary government and the component unit or (2) management of the primary government has operational responsibility for the component unit. The primary government is considered to have operational responsibility if it is managing the day-to-day operations of the component unit.

b. When the component unit provides services entirely, or almost entirely, to the primary government or otherwise exclusively, or almost exclusively, benefits the primary government even though it does not provide services directly to it. The essence of this type of arrangement is similar to an internal service fund – the goods or services are provided to the government itself rather than to the citizenry.

c. The component unit is organized as a not-for-profit corporation in which the primary government is the only corporate member.

d. The component unit’s outstanding debt or leases are expected to be repaid entirely or almost entirely from the resources of the primary government.

If a component unit does not meet criteria for blending, it should be presented discretely.